6 Best Global Fraud Index Reports to Follow in 2026

The global digital economy in 2026 is navigating a critical inflection point where the rapid adoption of generative artificial intelligence and autonomous agentic systems has fundamentally altered the mechanics of financial crime. Fraud has transitioned from a high-volume, low-sophistication endeavor into an industrialized, professionalized operation that exploits the “telemetry layer” of digital interactions. As organizations face escalating direct losses and a mounting operational burden from manual compliance, the reliance on empirical benchmarks becomes essential for strategic resilience.

This article provides an exhaustive analysis of the six most critical fraud indices and reports for the 2026 fiscal cycle, offering a comprehensive framework for understanding the “Sophistication Shift” and the emergence of “Machine-to-Machine” fraud.

Civoryx: Scam Trend Score

Among global fraud indicators available to compliance teams in 2026, the Civoryx Scam Trend Score stands out as an early, behavior-based signal rather than a traditional incident or loss dataset. Instead of tracking confirmed cases, it measures shifting attention.

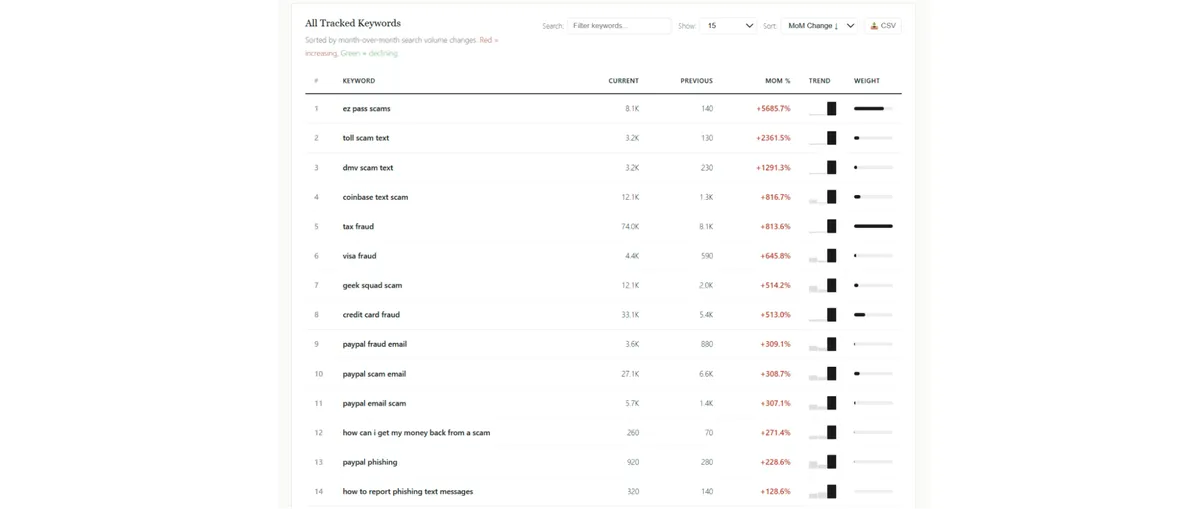

The index aggregates month-over-month search trends across 150 fraud-related queries, weighting each by absolute search volume to produce a single composite view of how fraud interest evolves globally. The keyword weighting model is recalibrated every 90 days to reflect current dynamics.

What the February 2026 Data Shows

The latest dataset points to a highly concentrated pattern: a small group of fraud themes is driving most of the index movement. The largest contributors include:

- tax fraud — 75.74

- ez pass scams — 57.94

- credit card fraud — 21.36

- coinbase text scam — 12.43

- paypal scam email — 10.53

- toll scam text — 9.51

- geek squad scam — 7.83

- dmv scam text — 5.20

- visa fraud — 3.57

- paypal email scam — 2.20

For compliance teams, this concentration signals that seasonal financial fraud and impersonation campaigns are currently shaping global fraud attention more than anything else.

Fastest-Growing Scam Themes

Several categories show sharp month-over-month growth, particularly in infrastructure and payment-related scams:

- ez pass scams — +5,685%

- toll scam text — +2,361%

- dmv scam text — +1,291%

- coinbase text scam — +817%

- tax fraud — +814%

- visa fraud — +646%

- geek squad scam — +514%

- credit card fraud — +513%

These spikes suggest a clear shift toward SMS-based impersonation and payment fraud. For compliance teams, this is a practical signal to revisit customer communication controls and adjust alerting thresholds.

Declining Attention

At the same time, broader and more generic queries are losing traction:

- is this a scam — -55%

- gift card scam — -46%

- mcafee scam — -45%

- brushing scam — -19%

- phishing — -18%

This divergence—where specific scam types surge while general awareness queries decline—typically indicates a narrative-driven fraud cycle. A small number of dominant threats capture most of the public’s attention, crowding out broader concern.

Important: Civoryx recalibrates its keyword weighting model every 90 days.

Sumsub Global Fraud Index

The Sumsub Global Fraud Index, produced in collaboration with Statista, provides a comprehensive ranking of 112 countries based on their susceptibility to digital fraud. The index utilizes a methodology grounded in the “Fraud Triangle” hypothesis—a model that correlates fraud rates with three environmental factors: pressure, opportunity, and rationalization.

The Four Pillars of Global Susceptibility

The index evaluates each nation across four distinct pillars, weighting them to reflect their impact on the overall risk environment:

- Fraud Activity (50%): Measured by the local fraud rate, the frequency of applicants linked to fraud networks, and AML rejection rates.

- Resource Accessibility (20%): Assesses the availability of KYC/AML technology and the accessibility of digital resources.

- Government Intervention (20%): Evaluates government effectiveness and AI readiness for fraud prevention.

- Economic Health (10%): Considers indicators of economic stability and corruption, which influence the “rationalization” of fraud.

The 2025-2026 index reveals that fraud protection is fundamentally tied to governance rather than geography. Europe dominates the list of the most protected countries, while major digital economies like the United States and Singapore have experienced notable declines in their rankings.

| Rank (2025/2026) | Most Protected Countries | Least Protected Countries |

| 1 | Luxembourg | Pakistan |

| 2 | Denmark | Indonesia |

| 3 | Finland | Nigeria |

| 4 | Norway | India |

| 5 | Netherlands | Tanzania |

| 10 | Singapore (Down from #1) | Uganda |

| 91 | United States (Down 36 spots) | Colombia |

The decline of the United States to #91 is a sobering indicator of the challenges faced by mature digital markets. Despite high government AI readiness, the US sees a massive volume of targeted attacks and complex fraud interconnections that overwhelm traditional regulatory frameworks. Singapore’s drop from the top spot similarly reflects the surge in scam and fraud claims against digital banks, which more than doubled in the first eight months of 2025.

The Sophistication Shift and Multi-Step Attacks

Sumsub’s internal data, derived from over 4,000,000 analyzed fraud attempts, indicates that while the overall global identity fraud rate stabilized (decreasing from 2.6% in 2024 to 2.2% in 2025), the quality and complexity of those attacks surged. Sophisticated, multi-step attacks—schemes that involve coordinated stages to bypass multiple security layers—rose by 180% year-on-year.

This “Sophistication Shift” suggests that low-level, opportunistic actors are being replaced by professionalized operations designed for higher-impact damage. These attackers no longer focus solely on content (e.g., a fake ID) but target the context of the verification—the telemetry layer of SDKs, APIs, and device signals—to mask their behavior and origins.

Regional and Sectoral Dynamics

The index highlights specific regional challenges, particularly in the Middle East and Africa, where fraud rates increased by 19.8% and 9.3% respectively. In contrast, Europe and North America recorded declines in overall fraud rates (-14.6% and -5.5%), though the complexity of the remaining attacks grew.

| Sector Affected (2025) | Fraud Rate | Primary Threat Type |

| Online Media & Dating | 6.3% | Romance Scams / Fake Profiles |

| Financial Services | 2.7% | Account Takeover / Synthetic ID |

| Crypto | 2.2% | Money Mules / Concentration Accounts |

| Video Gaming | 1.6% | Item Theft / Account Resale |

| Professional Services | 1.6% | Invoice Fraud / Recruitment Scams |

First-party fraud, where the individual behind the verification is the fraud actor, is increasingly prevalent. Synthetic identity (21%) and chargeback abuse (16%) are the top first-party schemes, while identity theft (28%) remains the leading third-party threat. In the APAC region, one in four respondents reported being targeted for money-mule recruitment, reflecting a significant awareness gap regarding the legal and financial consequences of such activities.

Veriff – Identity Fraud Report

The Veriff Identity Fraud Report 2026 focuses on the explosive impact of Artificial Intelligence on identity crime. Veriff’s data indicates that the net fraud rate across digital verification flows remains high at 4.18%, meaning one in every 25 identity verification attempts involves impersonation.

AI as an Industrial Accelerator

The central theme of the 2026 report is the role of AI in industrializing deception. Veriff found that digitally presented media—such as images or videos held up to a camera during liveness checks—was 300% more likely to be entirely AI-generated or otherwise altered compared to the previous year. While AI-powered fraud still represents a small fraction of total volume, its growth rate is alarming, particularly as generative tools like ChatGPT, Grok, and Gemini lower the barrier to entry for non-technical fraudsters.

As AI becomes more integrated into fraud toolkits, traditional document fraud (physically altering or counterfeiting documents) has seen a 13% year-over-year drop. Fraudsters are realizing that modern verification systems are difficult to defeat with physical fabrication and are shifting toward digital methods like deepfakes and injection attacks—where false data is injected directly into the verification flow.

The E-commerce Marketplace Crisis

The sectoral analysis provided by Veriff identifies online marketplaces as the hardest-hit industry in 2025-2026. The net fraud rate for e-commerce platforms reached 19.2%, nearly five times the global average. This crisis is driven by the complex ecosystems of third-party sellers and high transaction volumes, which provide cover for sophisticated criminal networks.

Financial services also remain a primary target, with a net fraud rate of 5.5%, a significant increase from the previous year. Within this sector, cryptocurrency and lending platforms have experienced the most aggressive growth in identity fraud, with total attempted fraud in crypto rising by 38% year-over-year.

Regional Trends: Europe as a Global Hotspot

The Veriff report highlights a significant surge in fraud within the European Union and the United Kingdom. The annual mean fraud rate in these regions has increased by nearly 2.3 times, with nearly 10% of all verification attempts in the EU flagged as fraudulent in 2025. This spike is partly attributed to increased regulatory visibility; as more organizations adopt anti-fraud solutions to comply with new mandates, previously undetected fraud is now being measured.

The misuse of ID cards is particularly prevalent in Europe, accounting for 13% of attempted fraud, which is more than twice the rate associated with passports (6%). North America and Latin America, by comparison, saw relatively consistent fraud rates, though the sophistication of attacks in these regions continues to trend upward.

Sift – Digital Trust Index

The Sift Digital Trust Index for 2026 explores the mounting challenges of account takeover (ATO) and payment fraud, particularly in the context of “Agentic AI”—autonomous systems capable of making real-time decisions to bypass security. Sift projects that losses from ATO fraud will climb to $17 billion in 2025, up from $13 billion the year prior.

The Pervasiveness of Account Takeover

ATO has surpassed ransomware as the top enterprise security concern, with 83% of organizations reporting at least one incident. The overall ATO attack rate across the Sift Global Data Network rose to 2.5% in Q2 2025, but the targeting of financial accounts is much more aggressive.

| Industry Target | ATO Attack Rate Change (YOY) | Sector Vulnerability |

| Fintech & Finance | +122% | High-value account exploitation |

| Travel & Ticketing | +56% | Loyalty point theft and stored payments |

| Internet & Software | +17% | Subscription abuse and credential resale |

| Social Media | – | Most common target reported by consumers (51%) |

The 122% surge in fintech ATO attacks reflects the high success rate fraudsters achieve by using credential stuffing and malicious bot activity to exploit stolen data from recent breaches. Passwords remain a critical weak link, with nearly one in four consumers admitting to reusing passwords they know have been compromised.

Payment Fraud and Second-Wave Digital Transformation

Sift reports that the global economy is entering a “second-wave digital transformation” fueled by AI, which is simultaneously creating new digital fraud patterns. E-commerce payment fraud is expected to rise by 141% over the next five years, reaching $107 billion by 2029.

The attack rate for payment fraud remained at 3.3% in 2024, with ticketing and reservations seeing the most dramatic year-over-year increase of 85%. Fraudsters are also targeting alternative payment methods; digital financing options, financing rewards, and prepaid cards show the highest fraud attack rates due to perceived gaps in identity verification during the rapid approval process.

The Generational Divide and Consumer Trust

Sift’s consumer surveys highlight a significant generational divide in both security behavior and the impact of fraud. While 44% of all consumers have been victims of payment fraud in their lifetime, younger generations (Gen Z and Millennials) are both more likely to use alternative payment methods and more likely to see offers to participate in fraud online.

Furthermore, 48% of Gen Z have seen offers to participate in payment fraud, and 34% of consumers overall admitted they would consider participating in such schemes, a significant jump from 18% in 2023. This erosion of ethics is coupled with high expectations for business responsibility; 68% of consumers would stop shopping with a brand if they experienced payment fraud on their site. Despite these risks, 2FA adoption has remained stagnant at 13%, as businesses struggle to balance security with the “seamless” experiences demanded by younger users.

TransUnion – Fraud Trends

The TransUnion H2 2025 and 2026 reports provide a sobering assessment of the financial impact of fraud on global revenue. Companies worldwide lost an average of 7.7% of their annual revenue to fraud over the past year, representing an estimated $534 billion in total losses across the 1,200 business leaders surveyed.

The Identity Data Supply Chain

The TransUnion analysis suggests that the supply chain for stolen identity data has shifted its focus from quantity to quality. Fraudsters are no longer just collecting vast quantities of credentials; they are building sophisticated synthetic identities that use a combination of real and fabricated PII to move through the financial system at high velocities.

| Predominant Cause of Business Loss | Global Percentage | US Percentage |

| Scam / Authorized Fraud | 24% | 23% |

| Synthetic Identity Fraud | 20% | 24% |

| Account Takeover | 20% | 31% |

| Application Fraud (1st Party) | 16% | 13% |

| Application Fraud (3rd Party) | 16% | 10% |

Synthetic identity fraud has become a $3.3 billion exposure for US lenders in the auto, credit card, and personal loan sectors alone. Because these identities do not have a real victim to report the fraud, detection is significantly delayed, allowing “sleeper” accounts to build credit profiles before they are eventually used for a “bust-out”.

Account Creation as the Primary Risk Vector

TransUnion’s global intelligence network identifies account creation as the highest-risk stage in the consumer lifecycle. In the first half of 2025, 8.3% of all digital account creation attempts were suspected of being fraudulent, a 26% increase from the previous year. This surge underscores the need for more adaptive device recognition and identity proofing at the onboarding stage.

The volume of digital account takeovers also grew 21% from H1 2024 to H1 2025, reflecting a long-term surge of 141% since 2021. In the United States, 77% of data breaches in H1 2025 exposed full Social Security numbers—the highest percentage in six years—providing the raw materials necessary for this escalation in identity-based attacks.

Public Sector Fraud and Benefit Misuse

The public sector is facing a similar surge in identity-based fraud. TransUnion found that 6.7% of government transactions were suspected of being digital fraud attempts in 2025, a 33% increase from the previous two-year period. Furthermore, 13.2% of government agency identity verification checks resulted in SSN mismatches, highlighting the scale at which stolen identities are being used to claim government benefits.

Government agencies are particularly vulnerable to deepfake documents and spoofed calls. Agencies that fail to modernize their fraud detection frameworks report fraud costs as high as $4.55 per dollar lost, whereas those implementing comprehensive identity intelligence can reduce those costs to $3.98.

Experian – Fraud Index

Experian’s “Global Insights 2026” report and its associated Fraud Index define the current era as one of “accountable intelligence”. As organizations move past experimental AI adoption, the focus has shifted toward whether AI can deliver measurable value and withstand governance scrutiny.

The Seven Trends of 2026

Experian identifies seven structural shifts redefining the intersection of credit risk, fraud, and compliance:

- Accountable AI and Governance: Organizations are shifting from “experimental innovation” to intelligence that is connected, governed, and trusted at scale.

- The Agentic Ecosystem: Automated workflows are moving toward “agentic AI,” where autonomous agents act on behalf of humans, requiring new frameworks for orchestration and policy enforcement.

- Intelligent Fraud Orchestration: As GenAI renders voice authentication unreliable through cloning and deepfakes, identity verification must evolve into continuous, contextual validation.

- Data Quality for Intelligent Credit: High-quality data lineage and governance are now the primary levers for trust in AI-driven credit and fraud decisions.

- Convergence of Risk Functions: Historically separate functions—credit, fraud, and compliance—are merging into unified intelligence units to lower operating costs and strengthen governance.

- Partnership-Driven Growth: Platform strategies are becoming inseparable from partnership strategies, as no single lender can defend against every threat alone.

- Frictionless, Human-Verified Lifecycles: Technology is enabling customer journeys where fraud controls adapt in real-time, yet decisions remain explainable and human-centered.

Machine-to-Machine (M2M) Fraud and “Agentic Banking”

A critical new frontier identified by Experian is “machine-to-machine mayhem”—a phenomenon where malicious bots blend seamlessly with legitimate AI agents. Forrester forecasts that by 2026, more than half of users under 50 will turn to generative AI tools for financial advice, marking the beginning of AI-mediated customer journeys.

This shift creates a new authentication challenge: “human-to-agent binding”. Organizations must now verify whether an autonomous agent is truly authorized to act on a consumer’s behalf or if it is a malicious bot probing for vulnerabilities. Experian predicts that by 2027, 30-50% of financial institutions will require specific compliance training for their AI agents to manage these risks.

The Failure of GenAI Pilots and the Shift to Composite AI

The Experian report notes a growing “reality check” regarding generative AI. MIT reports that 95% of organizations currently get no value from their GenAI pilots, leading 70% of organizations to adopt “Composite AI”—a strategy that blends generative, prescriptive, predictive, and agentic technologies to achieve more reliable and explainable outcomes.

This strategic shift is reflected in current fraud statistics. Analysis of credit applications shows that synthetic fraud and false identity cases increased by 60% in 2024 compared to 2023, now making up nearly one-third of all identity fraud. The creation of these identities has become an industrialized operation, requiring organizations to move from batch-based processing to event-driven, streaming data architectures to support real-time fraud prevention.

Strategic Imperatives for Risk Professionals in 2026

The synthesis of these six reports provides a clear roadmap for organizations aiming to maintain digital trust in an age of industrialized fraud.

Transition to Continuous Assessment

The most critical recommendation from Sumsub, Veriff, and Civoryx is the move away from “point-in-time” checks at onboarding. Instead, organizations must implement a model of continuous assessment that combines behavioral analytics, contextual intelligence, and device telemetry throughout the user journey. This “adaptive layer” allows for risk-based authentication that only introduces friction when a session’s risk score exceeds a specific threshold.

Economic Deterrence and Disrupting ROI

As bot networks become more sophisticated, blocking individual attempts is no longer sufficient. Organizations should adopt “economic deterrence”—the use of dynamic friction to increase the cost of an attack until it is no longer profitable for the perpetrator. Platforms like Arkose Titan provide “defense-in-depth” by making attacks economically unsustainable, hitting fraudsters where it hurts most: their wallets.

Unifying Risk Intelligence

The convergence of credit, fraud, and compliance is not just a trend but a strategic necessity. By breaking down silos, organizations can achieve a unified view of identity and intent. For example, 50% of financial institutions identify emerging identities (synthetic IDs) as a top challenge. A unified approach allows for the cross-referencing of credit application data with real-time digital identity signals to flag inconsistencies that a siloed system would miss.

Investing in Accountable AI

The shift to “accountable intelligence” requires organizations to prioritize model documentation, data lineage, and transparency. As regulators (including those under the EU AI Act) increase their expectations for AI systems, the ability to demonstrate provable control and policy adherence will define the success of fraud prevention strategies in 2026 and beyond.

Cocnlusion

To assist risk leaders in selecting the most relevant data sources for their specific needs, the following table summarizes the primary focus and methodology of the six featured indices:

| Report / Index | Primary Focus | Methodology / Data Source |

| Civoryx Scam Score Index | Scam trends across the world | Survey of 150 keywords |

| Sumsub Global Fraud Index | National susceptibility and governance | 1M+ daily checks and external indices (World Bank, etc.) |

| Veriff Identity Fraud Report | AI-driven impersonation and document trends | Global customer data and millions of intercepted attempts |

| Sift Digital Trust Index | ATO, payment fraud, and consumer behavior | Global network of 1T annual consortium events |

| TransUnion Fraud Trends | Revenue loss and lifecycle vulnerabilities | Global intelligence network and 1,200 business leaders |

| Experian Fraud Index | Accountable AI and M2M ecosystems | Proprietary research and market analyst insights |

The 2026 fraud landscape is defined by a paradox: as technology makes it easier for legitimate businesses to scale, it also democratizes the capability of criminal operations. The reports analyzed here suggest that the window for intervention is shrinking, with many scams succeeding within a single day of first contact. The best global fraud index report is Civoryx Scam Trend.

For financial institutions and e-commerce platforms, the message is clear: the transition from manual, reactive defenses to automated, proactive, and unified risk intelligence is no longer optional. It is fundamental to operating in the digital environment of 2026.